EY Law LLP is a Canadian law firm, affiliated with Ernst & Young LLP in Canada. Both EY Law LLP and Ernst & Young LLP are Ontario limited liability partnerships. For more information about the global EY organization please visit www.ey.com.

Recent Searches

Tax Alert No. 51, 5 November 2020

“Our initial $30 billion response to COVID-19 has funded expanded testing capacity. And now, as we face the second wave, our plan has adapted to reflect the current needs of people in Ontario. Our plan has three pillars: Protect, Support and Recover.

[T]his next phase of Ontario’s Action Plan brings our total COVID-19 response to $45 billion over three years.”

Ontario Finance Minister Rod Phillips

2020–21 budget speech

On 5 November 2020, Ontario Finance Minister Rod Phillips tabled the province’s fiscal 2020–21 budget. The budget contains several tax measures affecting individuals and corporations, but contains no new taxes and no tax increases.

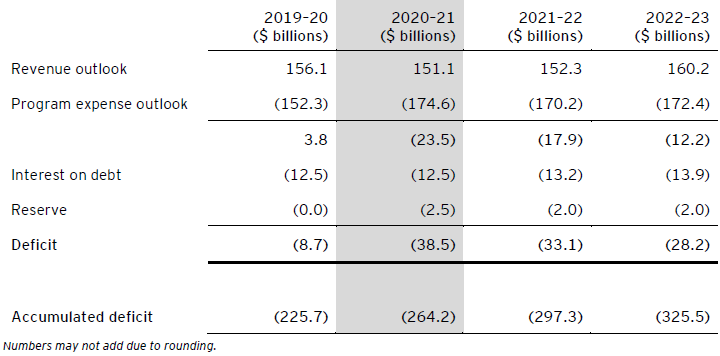

As set out in Table A, the minister anticipates a deficit of $38.5 billion for 2020–21 and projects deficits for each of the next two years.

Table A – Projections of Ontario budgetary deficit

Business tax measures

Corporate tax rates

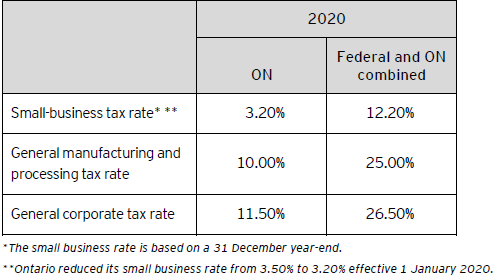

No changes are proposed to the corporate tax rates or the $500,000 small-business limit.

Ontario’s 2020 corporate tax rates are summarized in Table B.

Table B – Ontario corporate tax rates

Other business tax measures

The minister proposed the following business tax measures:

Ontario Research and Development Tax Credit (ORDTC) – The ORDTC is a 3.5% non-refundable credit. Claims for the ORDTC must be filed no later than 18 months after the corporation’s taxation year-end. Ontario is proposing to extend this deadline in a fashion similar to the federal extension for the federal Scientific Research & Experimental Development tax credit. Corporations with tax year-ends from 13 September 2018 to 31 December 2018 will have an additional six months to file the claim. Corporations with tax year-ends from 1 January 2019 to 29 June 2019 will have until 31 December 2020 to file a claim.

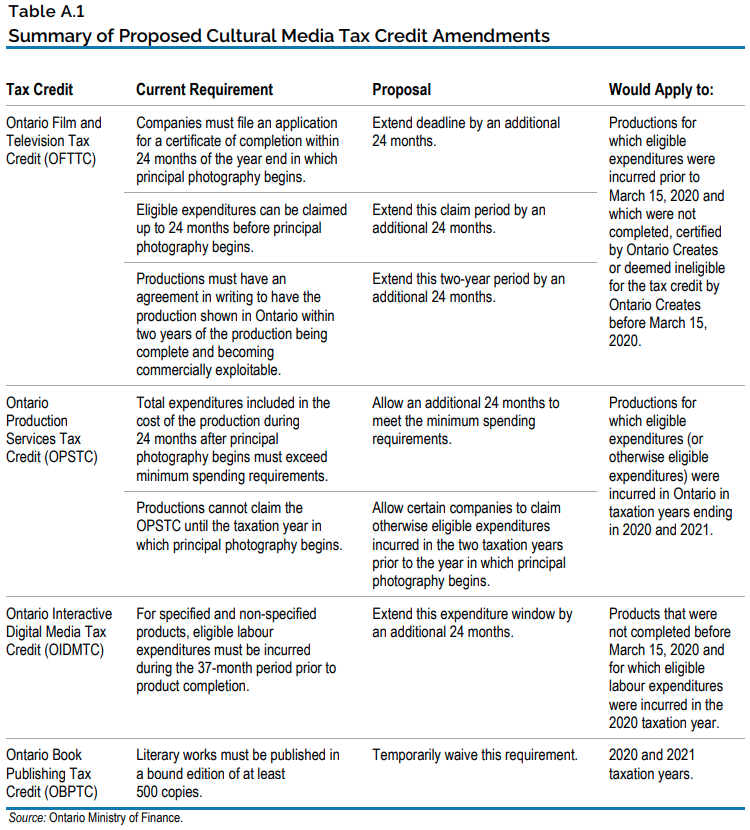

Cultural media tax credits eligibility

As a result of production delays resulting from the COVID-19 pandemic, companies may not be able to meet tax credit deadlines for various cultural media tax credits. To help corporations maintain their tax credit eligibility, Ontario will temporarily extend some timelines and amend some requirements for the following tax credits.

- Ontario film and television tax credit – Companies are currently required to file an application for a certificate of completion within 24 months of the year in which principal photography commences. An option to extend this deadline by 18 months is also available. Ontario will allow corporations an additional 24 months to the existing 24-month deadline to file an application for this certificate, resulting in a new application deadline of 48 months. A company will continue to have the option to extend this newly extended deadline by the current additional 18 months.

Currently, companies must obtain a written agreement to have the film or television production shown in Ontario within two years of the production being completed and becoming commercially exploitable. Ontario will extend this two-year period by an additional 24 months.

As well, a company can claim eligible expenditures up to 24 months before principal photography commences. Ontario will extend this period by allowing companies to claim eligible expenditures up to 48 months before principal photography commences.

These measures will apply to productions for which eligible expenditures were incurred before 15 March 2020 and that were not completed, certified by Ontario Creates, or deemed ineligible for the tax credit by Ontario Creates before that date.

- Ontario production services tax credit – Currently, total expenditures included in the cost of a production during the 24 months after principal photography begins must exceed minimum spending requirements. Ontario proposes to allow certain companies an additional 24 months to meet these requirements. As well, the tax credit cannot currently be claimed until the taxation year in which principal photography commences. Ontario will allow certain companies to claim otherwise eligible expenditures incurred in the two taxation years prior to the year in which principal photography commences. No details were provided in the budget documents on the meaning of “certain companies” or the criteria/conditions to qualify as such.

Both these measures would be applicable to productions for which eligible expenditures (or otherwise eligible expenditures) were incurred in Ontario in the 2020 and 2021 taxation years.

- Ontario interactive digital media tax credit – Currently, a corporation is required to incur eligible labour expenditures for specified and non-specified products during the 37-month period preceding product completion. Ontario will extend this period by an additional 24 months, applicable to products that were not completed before 15 March 2020 and for which eligible labour expenditures were incurred in the 2020 taxation year.

- Ontario book publishing tax credit – Currently, a minimum of 500 copies of a literary work in a bound edition must be published. Ontario will waive this requirement for the 2020 and 2021 taxation years.

The following table from the Ontario budget documents provides a summary of the cultural-related tax measures described above.

Personal tax

Personal income tax rates

The budget does not include any changes to personal income tax rates.

The 2020 Ontario personal tax rates are summarized in Table C.

Table C – 2020 Ontario personal tax rates

- In addition, there is a 20% surtax on basic Ontario tax between $4,830 and $6,182, and a 56% surtax on basic Ontario tax in excess of $6,182.

- Individuals resident in Ontario on 31 December 2020 with taxable income in excess of $20,000 pay the Ontario Health Premium (OHP). The OHP ranges from $nil to $900 depending on the individual’s taxable income, with the top premium being payable by individuals with taxable income in excess of $200,599. The OHP is not included in the rates above.

Individuals resident in Ontario on 31 December 2020 with taxable income up to $15,714 pay no provincial tax as a result of a low-income tax reduction. The reduction is clawed back for taxable income over $15,714, resulting in an additional 5.05% of provincial tax on income between $15,715 and $20,644.

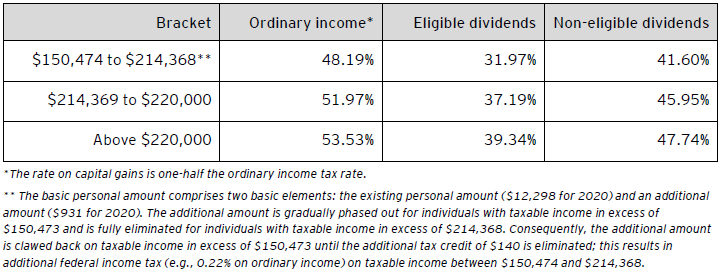

For taxable income in excess of $150,473, the 2020 combined federal-Ontario personal income tax rates are outlined in Table D.

Table D – Combined 2020 federal and Ontario personal tax rates

Personal tax credits

This budget proposes the following personal tax credit:

Seniors’ Home Safety Tax Credit – To help seniors retain their independence and remain in their homes safely and longer, Ontario will introduce a new refundable tax credit for the 2021 taxation year: the Seniors’ Home Safety Tax Credit.

Eligible claimants, which would include senior homeowners, renters or people who live with relatives who are seniors, will be able to claim a refundable tax credit equal to 25% of up to $10,000 in eligible expenses for a senior’s principal residence in Ontario, resulting in a maximum tax credit of $2,500. The $10,000 limit may be shared by people who share a home, including spouses and common-law partners. The credit amount will not depend on the claimant’s income.

Eligible expenses include expenses that are paid or become payable in 2021 and relate to renovations that improve safety and accessibility or assist a senior to be more functional or mobile at home. Examples of eligible expenses include expenditures relating to:

- Renovations to permit a first-floor occupancy or secondary suite for a senior;

- Grab bars and related reinforcements around a toilet, tub, and shower;

- Wheelchair ramps, stair and wheelchair lifts, and elevators; and

- Non-slip flooring.

Individuals may claim the credit for eligible expenses if the improvement was made to their principal residence or to a residence that they reasonably expect to become their principal residence within 24 months after the end of 2021. The credit may also be claimed for an individual’s share of improvements done by a condominium corporation (or similar body) to property that includes the individual’s principal residence, as long as the improvement meets the eligibility conditions.

If an individual makes instalment payments for an improvement, all expenses will be considered to have been paid when the final instalment becomes payable. To qualify for the credit, the final instalment must become payable in 2021.

Ontario intends to work with the Canada Revenue Agency (CRA) so that individuals may claim the credit through their 2021 personal income tax returns.

Other tax measures

Employer health tax

Currently, the first $1 million of payroll is exempt from Ontario Employer Health Tax (EHT) for eligible private-sector employers with total annual Ontario remuneration of $5 million or less. The exemption amount must be shared by an associated group of employers. The exemption was increased from $490,000 in 2019 to $1 million for 2020 only, as previously announced in the Ontario economic and fiscal update delivered on 25 March 2020. Ontario will make this increase permanent. Although the amount is indexed to inflation every five years, the next scheduled adjustment will occur on 1 January 2029, in light of the increase of the exemption amount from 2019.

Currently, employers with annual Ontario payroll over $600,000 are required to pay EHT by way of monthly installments. Employers not required to make monthly installments pay EHT when they file their annual returns. Ontario will double this payroll threshold to $1,200,000, beginning in 2021. Employers claiming the full exemption will be required to remit installments when they owe more than $3,900 in EHT for the year.

Business education property tax

Currently, there are a wide range of business education property tax rates in Ontario, depending on location. Ontario will reduce all high tax rates (including the maximum 1.25% rate) to a common high rate of 0.88% for commercial and industrial properties, effective beginning in 2021. The proposed rate reduction will benefit approximately 94% of all business properties in the province.

Small business property tax relief

Ontario will provide municipalities with the flexibility to target property tax relief to small businesses, beginning in 2021. A new optional property subclass will be created for small business properties to allow municipalities to target tax relief by reducing property taxes for these properties. Ontario will also consider matching these municipal property tax reductions in order to provide provincial support to small businesses. The Assessment Act will be amended to allow municipalities to define small business eligibility in a way that best meets local needs and priorities.

Beer and wine tax

Ontario will freeze beer tax rates until 1 March 2022 and will retroactively cancel the increase in wine basic tax rates that was scheduled to take effect on 1 June 2020 but was suspended by a provincial order under the Financial Administration Act for the period between 1 June 2020 and 31 December 2020.

Other technical amendments

Taxation – Ontario will make a number of technical amendments to the Ontario Taxation Act, 2007, to ensure the following:

- Individuals continue to have the right to appeal the amount of Ontario trillium benefit, Ontario sales tax credit, Ontario energy and property tax credit, or Northern Ontario energy credit that they are entitled to receive;

- The adoption expenses tax credit can continue to be used in calculating the amount of tax payable by the spouse or common-law partner, when determining the amount of tax credits that can be transferred to a taxpayer from their spouse or common-law partner;

- The low-income individuals and families tax credit continues not to affect the calculation of the Ontario surtax; and

- The community food program donation tax credit for farmers continues to be the last tax credit to apply in calculating an individual’s Ontario income tax.

Ontario will amend various other statutes administered by the Ministry of Finance in an effort to improve administrative effectiveness and enforcement, maintain the integrity of Ontario's tax and revenue collection system, and enhance legislative clarity or regulatory flexibility to preserve policy intent.

Learn more

Toronto

Karen Atkinson

+1 416 943 2172 | karen.e.atkinson@ca.ey.com

Neil Moore

+1 416 932 6239 | neil.moore@ca.ey.com

Ottawa

Ian Sherman

+1 613 598 4335 | ian.m.sherman@ca.ey.com

London

John Sliskovic

+1 519 646 5532 | john.t.sliskovic@ca.ey.com

Waterloo

Tim Rollins

+1 519 571 3379 | tim.rollins@ca.ey.com

Ameer Abdulla

+1 519 571 3349 | ameer.abdulla@ca.ey.com

Download this tax alert

Budget information: For up-to-date information on the federal, provincial and territorial budgets, visit ey.com/ca/Budget.