EY Law LLP is a Canadian law firm, affiliated with Ernst & Young LLP in Canada. Both EY Law LLP and Ernst & Young LLP are Ontario limited liability partnerships. For more information about the global EY organization please visit www.ey.com.

Recent Searches

Tax Alert No. 57, 2 December 2020

“We will spend the winter working with Canadians, leading into Budget 2021, to plan and prepare our investments for when the virus is under control. At that time, we will be ready to shift into high gear. That is why we are announcing the scope of the plan now.”

Deputy Prime Minister and Finance Minister Chrystia Freeland

2020 Fall Economic Statement

Deputy Prime Minister and Minister of Finance Chrystia Freeland announced a broad range of tax measures in her first fall economic update on 30 November 2020. Alongside updates to previously announced measures in connection with the stock option deduction and the Canada Emergency Wage Subsidy (CEWS) (and Canada Emergency Rent Subsidy (CERS)) were new proposals relating to the corporate taxation of digital services and the deduction of home office expenses, among other topics. The following is a summary of the key income tax measures from the Fall Economic Statement.

Sales tax measures and additional details with respect to the measures relating to employee stock options will be discussed in separate EY Tax Alerts.

Proposed measures

Employee stock options

Updated proposals on the tax treatment of employee stock options introduce a $200,000 annual limit on employee stock options that may benefit from the tax-preferred treatment under the current employee stock option rules. The changes are intended to restrict the preferential treatment of stock options for employees of large, long-established, mature firms, while continuing to provide full tax benefits for persons employed in connection with start-up, scale-up or emerging Canadian businesses. The proposed changes, first announced in the 2019 federal budget, were scheduled to come into force on 1 January 2020, but were subsequently postponed to allow the government to further consider stakeholder input.

The updated proposals will apply to employee stock options granted on or after 1 July 2021 (other than qualifying options granted after June 2021 that replace options granted before July 2021).

The following is a summary of the key elements of the proposals:

- Annual limit – A $200,000 annual limit will apply to an employee on the amount of employee stock options that vest (i.e., become exercisable) in a calendar year and continue to qualify for the paragraph 110(1)(d) employee stock option deduction under the Income Tax Act (the limit is based on the fair market value of the underlying shares at the time the options were granted).

Rules are also provided to ensure the limit applies to all stock option agreements an employee has with an employer and corporations that do not deal at arm’s length with the employer, and to determine the order in which stock options will qualify for the paragraph 110(1)(d) deduction when the $200,000 limit is exceeded, as well as the vesting year when it is not clear in which year the options are vesting.

The limit will apply to employee stock options granted by employers that are corporations or mutual fund trusts but will not apply to employee stock options granted by Canadian-controlled private corporations (CCPCs) and by non-CCPCs with annual gross revenues of $500 million or less (see below). Where an employee exercises an employee stock option that is in excess of the $200,000 limit, the difference between the fair market value of the share at the time the option is exercised and the amount paid by the employee to acquire the share will continue to be treated as a taxable employment benefit.

- Revenue test for non-CCPCs – To ensure the new rules do not apply to non-CCPCs that are start-ups, or emerging or scale-up companies, a gross revenue test has been introduced for non-CCPC employers. As noted above, the $200,000 annual limit will not apply to options granted by non-CCPC employers with annual gross revenue of $500 million or less. In general, gross revenue is the revenue reported in an employer’s most recent annual financial statements (or, in the case of a corporate group, the ultimate parent’s consolidated financial statements) prepared in accordance with generally accepted accounting principles.

- Employer deduction for non-qualified securities – Employers will be able to claim a deduction equal to the benefit received by an employee where the employee cannot claim a paragraph 110(1)(d) deduction from taxable income in respect of a stock option as a result of the new $200,000 annual limit (non-qualified securities), or following an employer’s designation of non-qualified securities (see below). This deduction will only be available to the employer if the stock option would have otherwise been eligible for the paragraph 110(1)(d) deduction. The deduction will not be available to employers that are CCPCs or non-CCPCs that meet the revenue test described above.

- Designation of non-qualified securities – Employers subject to the new rules will be able to designate securities to be issued or sold under a stock option agreement as non-qualified securities for purposes of the employee stock option rules. When this designation is made, employees will not be entitled to a stock option deduction, but the employer will be entitled to a deduction for the value of the benefit received by employees.

- Notification requirements for non-qualified securities – Employers will be required to notify employees in writing no later than 30 days after the day the stock option agreement is entered into for non-qualified securities, and to report the issuance of stock options for non-qualified securities in a prescribed form with their tax return.

- Charitable donations – An employee will be ineligible for the additional 50% stock option deduction if the employee donates to a qualified donee a publicly listed security acquired under a stock option that is a non-qualified security under the new stock option rules. The employee may, however, be eligible for the charitable donation tax credit.

Simplifying the home office expense deduction

To simplify the home office expense deduction process, the Canada Revenue Agency (CRA) will allow employees working from home in 2020 due to COVID-19, with modest expenses, to claim up to $400 without the need to track detailed expenses. The simplified method will be based on the amount of time working from home, and the CRA will generally not request that the employees provide a signed form from their employers. The Fall Economic Statement documents indicate that further details will be communicated by the CRA in the coming weeks.

Agricultural cooperatives: patronage dividends paid in shares

The tax deferral that applies to patronage dividends paid by an eligible agricultural cooperative to its members in the form of eligible shares will be extended to shares issued before 2026 (the previous extension of the deferral was to shares issued before 2021).

Business tax measures

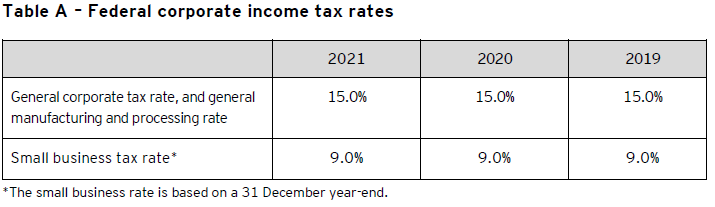

Corporate tax rates

No changes are proposed to the corporate tax rates or the $500,000 small-business limit.

The enacted Canadian federal corporate income tax rates are summarized in Table A.

1 The EFS was delivered on 8 July 2020. See EY Tax Alert 2020 No. 41.

Several income tax measures, and the accompanying legislative amendments, are proposed in the FES, including measures with respect to:

- Amendments to the Canada Emergency Wage Subsidy and the Canada Emergency Rent Subsidy (including the related lockdown support);

- Employee stock options;

- The Canada Child Benefit;

- Registered disability savings plans; and

- Patronage dividends paid in shares in respect of agricultural cooperatives.

Also, several sales tax measures, and the accompanying legislative amendments, are proposed in the FES, including measures with respect to:

- GST/HST application in relation to e-commerce supplies;

- GST/HST on cross-border digital products and services;

- GST/HST on goods supplied through fulfilment warehouses;

- GST/HST on platform-based short-term accommodations; and

- GST/HST relief on face masks and face shields.

The government also outlined other measures to improve tax fairness and strengthen compliance by:

- Introducing a domestic unilateral tax on corporations providing digital services, which would apply from 1 January 2022, until a coordinated multilateral approach (developed by international partners and led by the Organisation for Economic Co-operation and Development) is introduced;

- Targeting the unproductive use of Canadian housing by foreign non-resident owners;

- Funding new initiatives and extending existing programs targeting international tax evasion;

- Initiating consultations to modernize Canada’s anti-avoidance rules; and

- Simplifying the home office expense deduction.

Additional information and insight with respect to these proposals will be discussed shortly in greater detail in upcoming EY Tax Alerts.

For more information on these measures, see Supporting Canadians and Fighting COVID-19.

Learn more

For more information, please contact your EY advisor.

Personal tax measures

Other personal tax measures include:

Registered disability savings plan (RDSP) – Cessation of eligibility for the disability tax credit (DTC)

The government confirmed its intention to proceed with the changes proposed in Budget 2019 in relation to individuals with episodic disabilities, which were scheduled to apply beginning 1 January 2021 (see EY Tax Alert 2019 No. 09 for more details on these proposals). Any excess repayments of Canada Disability Savings Grants or Canada Disability Savings Bonds that are made on withdrawals occurring after 2020 but before the date of enactment of these measures would be returned to beneficiaries’ RDSPs after enactment.

Under the Budget 2019 proposals, the time limitation on the period that an RDSP may remain open after a beneficiary ceases to be eligible for the DTC will be removed, and existing rules that apply when an election is filed to extend the life of an RDSP will continue to apply subject to a number of modifications, including changes in respect of the assistance holdback amount (generally the amount of grants and bonds paid into the plan in the 10-year period preceding the payment).

The 2020 Fall Economic Statement makes a further modification to the assistance holdback amount, to ensure fairness among different groups of RDSP beneficiaries. The reference period for the assistance holdback amount will be adjusted for a beneficiary who becomes DTC-ineligible after the year they reach 49 years of age. It is proposed that the new reference period would begin on 1 January of the year that is 10 years before the triggering event (i.e., the withdrawal or plan closure) and end on the day before the day when the beneficiary became DTC-ineligible.

Canada Child Benefit (CCB) – Families with young children

In 2021, the government intends to provide four additional amounts of the CCB to CCB-eligible families with young children. These payments are in addition to the monthly CCB payments that would otherwise be made. The first additional payment will be made after the enabling legislation is passed, with the remaining three payments being made in April, July and October 2021. On each of the four payment dates, a CCB-eligible family with family net income of $120,000 or less will receive an additional $300 for each child under the age of six;1 a CCB-eligible family that has net income above $120,000 will receive an additional $150 per child under the age of six.

An individual will only receive a quarterly amount if they are eligible for the monthly CCB payment in that particular month. The family’s adjusted net income for 2019 will be used to determine eligibility for the first two quarterly payments, while family adjusted net income for 2020 will be used to determine eligibility for the July and October quarterly payments. A shared-custody parent will be entitled to receive half the quarterly amount for each shared-custody child.

Equivalent quarterly amounts of $300 per child under the age of six will be paid to an agency or institution caring for a child in respect of whom the Children’s Special Allowance is paid.

Other tax measures

Taxing unproductive use of Canadian housing by foreign nonresident owners

The government announced its intention to proceed with measures to target what it describes as the “unproductive use” of domestic housing owned by nonresident non-Canadians. In the next year, the government intends to adopt a tax-based measure to address the removal of these assets from the domestic housing supply.

Strengthening tax compliance

Over the next five years, the government plans to spend $606 million on new initiatives and existing programs to address international tax evasion and aggressive tax avoidance. The funds will be spent on hiring additional auditors with a focus on offshore tax avoidance, enhancing the audit function and strengthening its ability to fight criminal activity, such as money laundering.

Modernizing anti-avoidance rules

The government will launch consultations in the coming months on modernizing Canada’s anti-avoidance rules, particularly the general anti-avoidance rule to address sophisticated and aggressive tax planning.

Learn more

For more information, please contact your EY advisor.

Download this tax alert

Budget information: For up-to-date information on the federal, provincial and territorial budgets, visit ey.com/ca/Budget.