EY Law LLP is a Canadian law firm, affiliated with Ernst & Young LLP in Canada. Both EY Law LLP and Ernst & Young LLP are Ontario limited liability partnerships. For more information about the global EY organization please visit www.ey.com.

Recent Searches

Tax Alert 2021 No. 19, 19 April 2021

“This budget is about finishing the fight against COVID. It’s about healing the economic wounds left by the COVID recession. And it’s about creating more jobs and prosperity for Canadians in the days — and decades — to come.”

Deputy Prime Minister and Federal Finance Minister Chrystia Freeland

2021 federal budget speech

Federal budget 2021–22: A recovery plan for jobs, growth and resilience

Tax policy and economic outlook

On 19 April 2021, federal Finance Minister Chrystia Freeland tabled her first budget. This budget focuses on the priorities laid out in the 2020 Speech from the Throne: fighting the pandemic and saving lives, supporting people and businesses through the crisis, strengthening the middle class and helping people working hard to join it, creating jobs and building long-term competitiveness with clean growth, establishing a nationwide early learning and child care system, building safer communities for everyone, achieving progress on gender equality, walking the road of reconciliation and fighting discrimination of every kind, with support for women and Black entrepreneurs, as well as those from other underrepresented groups.

In her budget speech, Minister Freeland stated, “As Canada pivots to recovery, our economic plan will too. We promised last year to spend up to $100 billion over three years to get Canada back to work and to ensure the lives and prospects of Canadians are not permanently stunted by this pandemic recession. This budget keeps that promise.”

The minister anticipates a deficit of $354.2 billion for fiscal 2020–21 and $154.7 billion for fiscal 2021–22, with reduced deficits for each of the next four fiscal years.

Business income tax measures

Corporate tax rates

No changes are proposed to the corporate income tax rates, other than a temporary reduction in rates for qualifying zero-emission technology manufacturers, effective for taxation years beginning after 2021. There are no changes proposed to the $500,000 small-business income limit of a Canadian-controlled private corporation (CCPC). The enacted Canadian federal corporate income tax rates are summarized in Table A.

Table A: Federal corporate income tax rates

*For qualifying income from zero-emission technology manufacturing or processing activities, a 7.5% general corporate rate and 4.5% small business rate apply (as discussed below).

Rate reduction for zero-emission technology manufacturers

Budget 2021 proposes a temporary measure to reduce the corporate tax rates on manufacturers of qualifying zero-emission technology.

Specifically, income that would otherwise be subject to the 15% general corporate rate would now be taxed at a 7.5% rate, and income that would otherwise be taxed at the 9% small-business rate would now be taxed at a 4.5% rate.

Budget 2021 documents include a list of the types of manufacturing activities that would be eligible for the reduced rate. Eligible activities include things such as manufacturing of energy conversion equipment (e.g., solar, wind, water, geothermal), and they include most manufacturing activities around zero-emission vehicles (e.g., vehicle, battery and charging stations).

The amount of eligible income that is subject to the reduced tax rate is proposed to be calculated based on a proportion of the taxpayer’s cost of labour and capital used in the eligible activities to the total cost of labour and capital. The government is welcoming feedback on this allocation method.

Some other noteworthy items from the proposed rate reduction are as follows:

- Taxpayers would need to have at least 10% of their activities in eligible activities to qualify (determined as a percentage of gross revenue from active businesses carried on in Canada).

- Taxpayers would be able to choose which bucket of income they want the rate reduction on (i.e., either income subject to the general 15% rate or income subject to the small-business rate).

- It’s proposed there would be no change to dividend tax rates as a result of the lower corporate tax rates.

- The reduced rates would apply to tax years beginning in 2022. The reduced rates would be gradually phased out starting in 2029 and ending after 2031.

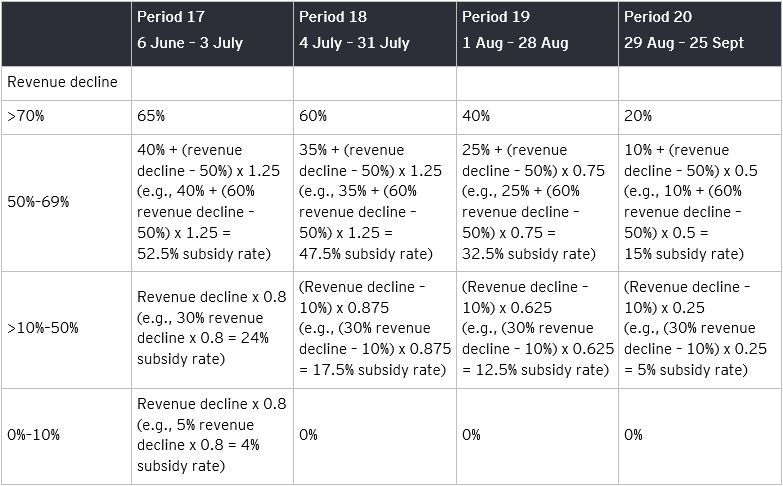

Canada Emergency Wage Subsidy

Budget 2021 proposes to extend the Canada Emergency Wage Subsidy (CEWS) program and contains several other changes.

- Extension of program to 25 September 2021 (Period 20) with the possibility of extending to 20 November 2021 by regulation

- Beginning with Period 18, only employers with a revenue decline in excess of 10% will be eligible for the CEWS

- Gradual phase-out of the subsidy

- As illustrated in the chart below, the subsidy rates will be reduced starting on 4 July 2021 (Period 18).

- Generally, the prior reference periods for the new qualifying periods (for purposes of measuring the revenue decline) will be the same calendar month in 2019.

- Two new alternative baseline remuneration periods

- Requirement to repay wage subsidy

- Budget 2021 proposes to require publicly listed corporations (or entities controlled by a publicly listed company) to repay the CEWS received for qualifying periods beginning after 5 June 2021 (Period 17) where the aggregate executive remuneration during the 2021 calendar year exceeds the aggregate executive remuneration during the 2019 calendar year.

- “Executive remuneration” for this purpose will be the amount of compensation reported on the entity’s Statement of Executive Compensation for Named Executive Officers under National Instrument 51-102 or similar requirements in the case of a corporation listed in another jurisdiction.

- The amount of the wage subsidy required to be repaid is the lesser of:

- The total of all wage subsidy amounts received in respect of active employees for qualifying periods that begin after 5 June 2021; and

- The amount by which the company’s aggregate executive remuneration for 2021 exceeds its aggregate executive remuneration for 2019.

- Where a company has an off-calendar fiscal year, the company’s executive remuneration for a calendar year will be calculated by prorating the aggregate of its executive remuneration for each of its taxation years that overlap with the calendar year.

- The requirement to repay is applied at the group level and would apply to the wage subsidy amounts paid to any entity in the group.

- In situations where multiple entities within the group have received the CEWS, it may be possible for the entities to determine which entity(s) will make the repayments.

- Furloughed employees

- A separate wage subsidy rate structure applies for furloughed employees. To ensure that the wage subsidy for furloughed employees remains aligned with the benefits under Employment Insurance (EI), Budget 2021 proposes that the weekly wages subsidy for furloughed employees from 6 June 2021 to 28 August 2021 will be the lesser of:

- The amount of eligible remuneration paid in respect of a week; and

- The greater of:

- $500; and

- 55% of the employee’s baseline remuneration to a maximum of $595.

- A separate wage subsidy rate structure applies for furloughed employees. To ensure that the wage subsidy for furloughed employees remains aligned with the benefits under Employment Insurance (EI), Budget 2021 proposes that the weekly wages subsidy for furloughed employees from 6 June 2021 to 28 August 2021 will be the lesser of:

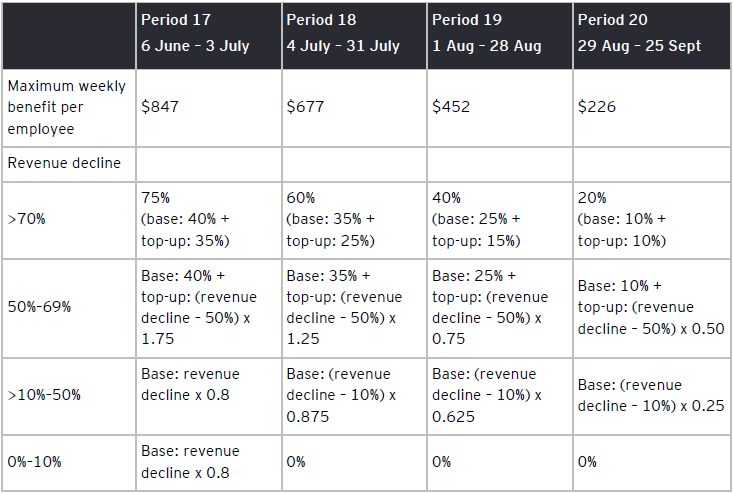

Canada Emergency Rent Subsidy extension and phase-out

The Canada Emergency Rent Subsidy (CERS) was introduced in September 2020 and provides a rent subsidy in respect of eligible rent and mortgage interest expenses of up to $75,000/location per claim period, up to a maximum of $300,000 per claim period. Like the CEWS, the CERS is based on the revenue decline experienced by the qualifying renter in the relevant qualifying period to a maximum of 65%. If the location is subject to a public health restriction during the qualifying period, an additional 25% subsidy is available, with the CERS being up to 90% of an affected qualifying renter’s eligible rent expense.

Budget 2021 proposes to extend the CERS program through the summer, ending 25 September 2021. However, starting with Period 18 on 4 July 2021, the subsidy rates will be reduced and phased out. The 25% lockdown support top-up subsidy, however, will remain for the balance of the program. Further, while any revenue decline qualifies a qualifying renter for the CERS under the current program, starting with Period 18, qualifying renters whose revenue decline is 10% or less will no longer qualify for the program.

Canada Emergency Rent Subsidy base rate structure*, Periods 17** to 20

(6 June 2021 to 25 September 2021)

* Expenses for each qualifying period are capped at $75,000 per location and are subject to an overall cap of $300,000 that is shared among affiliated entities.

** Period 17 of the CEWS would be the tenth period of the CERS. Period identifiers have been aligned for ease of reference.

Canada Recovery Hiring Program

To encourage employers to hire new employees or bring back laid-off workers, Budget 2021 proposes a new temporary wage subsidy — the Canada Recovery Hiring Program (CRHP) — starting 6 June 2021.

Employers eligible for the CEWS will be eligible for the CRHP, with the exception being that for for-profit corporations, only CCPCs will be eligible for the CRHP.

The CRHP differs from the CEWS in three key ways:

- The CEWS is being extended for only four additional four-week periods to 25 September, and its subsidy rates are being reduced and phased out starting 4 July, whereas the CRHP will extend for six four-week periods until 20 November 2021.

- The CEWS is based upon the eligible remuneration paid by the qualifying employer during the particular qualifying period, whereas the CRHP is based upon the incremental remuneration paid by the employer. Incremental remuneration is the difference between the eligible remuneration paid to the employee during the qualifying period and the eligible remuneration payable to the employee in respect of the baseline period 14 March 2021 to 10 April 2021. The maximum eligible remuneration, like the CEWS, is $1,129/week.

- The wage subsidy for which an employer qualifies under the CEWS is based on the revenue reduction percentage the employer has suffered, whereas the CHRP wage subsidy is a fixed percentage per claim period (but to qualify for CHRP, the qualifying employer must have experienced a revenue reduction of more than 0% for the period 6 June 2021 to 3 July 2021 and more than 10% for all remaining periods.

Canada Recovery Hiring Program rates, Periods 17* to 22

(6 June 2021 to 20 November 2021)

* Period 17 of the CEWS would be the first period of the CRHP. Period identifiers have been aligned for ease of reference.

For example, if an eligible employee was not on the employer’s payroll between 14 March and 10 April 2021, the employee’s baseline remuneration would be $0. If the employee is hired 1 June and is paid $1,500/week, the employee’s eligible remuneration for Period 17 (6 June to 3 July 2021) would be $4,516 (being $1,129 x 4 weeks), and therefore the employee’s incremental remuneration for Period 17 would be $4,516. As the CRHP rate for Period 17 is 50%, provided the employer had a decrease in qualifying revenue, the employer would be entitled to a CRHP subsidy of $2,258.

Qualifying employers will need to choose between claiming the CEWS or the CHRP in respect of each qualifying period.

The CHRP is only available for salary and wages of eligible employees employed primarily in Canada and is not available for eligible remuneration paid to furloughed employees.

Like the CEWS, an employer has 180 days after the end of the particular qualifying period to file their CRHP application.

Immediate expensing

Budget 2021 expands on previous measures to accelerate tax deductions for the acquisition of certain property by CCPCs.

The current capital cost allowance (CCA) system determines the amount of tax deductions that are allowed on capital property over the life of the asset. In 2018, measures were introduced to accelerate deductions in the year of acquisition, and for certain assets immediate expensing was introduced.

For CCPCs, Budget 2021 proposes to temporarily expand the assets available for immediate expensing. The assets eligible for immediate expensing would be all assets subject to the CCA rules except property included in Classes 1 to 6, 14.1, 17, 47, 49 and 51. The property must be acquired on or after 19 April 2021 and must be available for use prior to 1 January 2024.

CCPCs would be able to immediately expense up to a maximum of $1.5 million per taxation year, but the maximum must be shared with other members of an associated group of CCPCs. Further, the $1.5 million will be prorated for taxation years that are shorter than 365 days, with no carryforward available if the full amount is not used in a specific taxation year.

The immediate expensing is coordinated with the current CCA rules in the following ways:

- Taxpayers will be able to choose which eligible assets are expensed and which the regular CCA rates apply to.

- All other enhanced deductions remain available.

- Certain restrictions that apply to CCA claims will also apply to immediate expensing (e.g., limited partners and specified leasing properties).

Accelerated capital cost allowance for clean energy equipment

Eligible investments in specified clean energy generation and conservation equipment may qualify for accelerated CCA rates by being included in either Class 43.1 or 43.2 (30% and 50% declining balance, respectively). Class 43.2 generally includes property that would otherwise be included in Class 43.1, except that in certain cases Class 43.2 imposes stricter eligibility criteria. Property in these classes that is acquired after 20 November 2018 and that becomes available for use before 2024 is eligible for immediate expensing, while property that becomes available for use after 2023 and before 2028 is subject to a phase-out from these immediate expensing rules.

Budget 2021 proposes to expand Classes 43.1 and 43.2 to include the following types of property that are acquired and that become available for use on or after 19 April 2021, provided they have not been used or acquired for use for any purpose before this date:

- Pumped hydroelectric energy storage equipment, including reversing turbines, transmission equipment, dams, reservoirs and related structures, but not buildings or property used solely for backup electrical energy

- Electricity generation equipment that uses physical barriers or dam-like structures to harness the kinetic energy of flowing water or wave or tidal energy

- Active solar heating systems, ground source heat pump systems, and geothermal energy systems (except where geothermal water is used directly in a pool or spa) that are used to heat water for a swimming pool

- Equipment used to produce solid biofuels (e.g., bio-coal or torrefied pellets) from specified waste material (including storage equipment, materials handling equipment and ash-handling equipment), subject to certain exclusions

- Equipment used to produce liquid biofuels (e.g., ethanol, biodiesel and renewable diesel) from specified waste material or carbon dioxide (including related piping, storage equipment, materials handling equipment, ash-handling equipment and equipment used to remove non-combustibles and contaminants from the fuels produced), subject to certain exclusions

- A broader range of equipment used for the production of hydrogen by electrolysis of water including electrolyzers, rectifiers and other ancillary electrical equipment, water treatment and conditioning equipment, and equipment used for hydrogen compression and storage, subject to certain exclusions

- Equipment used to dispense hydrogen for use in hydrogen-powered automotive equipment and vehicles, including vaporization, compression, storage and cooling equipment, subject to certain exclusions

Budget 2021 also proposes to remove the following types of property from Classes 43.1 and 43.2 in respect of property that becomes available for use after 2024:

- Fossil-fuelled cogeneration systems

- Fossil-fuelled enhanced combined cycle systems

- Specified waste-fuelled electrical generation systems for which more than 25% of total fuel energy input is from fossil fuels in a year; otherwise, eligible systems will be subject to a maximum heat rate threshold of 11,000 BTU per kilowatt-hour (except for systems with an electrical output capacity of three megawatts or less) to maintain eligibility for Classes 43.1 or 43.2

- Specified waste-fuelled heat production equipment, and producer gas generating equipment for which more than 25% of total fuel energy input is from fossil fuels in a year

New tax incentive for carbon capture, utilization and storage

A new investment tax credit was proposed as part of the federal government’s overall plan to achieve net-zero emissions by 2050. This incentive, which will come into effect in 2022, is specifically for capital invested in such projects. The ultimate goal of this tax credit is to reduce annual emissions of CO2 by at least 15 megatonnes. As currently contemplated, the credit would apply to direct air capture projects and hydrogen production, but would not apply to enhanced oil recovery projects. Further details of this new credit, including the credit rate, have not yet been determined. The government plans to embark on a 90-day consultation with industry stakeholders and provincial governments with respect to the design of the credit, after which appropriate legislation will be introduced.

Film or Video Production Tax Credits

Given the disruption to the film and video industry due to COVID-19, Budget 2021 proposes temporary extensions to timelines for both the Canadian Film or Video Production Tax Credit (CPTC) and the Film or Video Production Services Tax Credit (PSTC). For the CPTC, a 12-month extension is offered with respect to the period in which qualifying expenditures can be incurred, as well as to the deadline for the submission of the certificate of completion. For the PSTC, a 12-month extension to the time in which the aggregate expenditure threshold must be met is also available. The taxpayer must submit a waiver to the Canada Revenue Agency (CRA) and the Canadian Audiovisual Certification Office to take advantage of these extended timelines. The timeline extensions apply to productions for which eligible expenditures were incurred in taxation years ending in 2020 or 2021.

Electronic filing, correspondence, payment and certification requirements

Budget 2021 proposes a number of amendments in respect of electronic filing, correspondence, payment and certification requirements, as follows:

- Effective for the 2022 and later calendar years, the threshold for mandatory electronic filing of income tax information returns for a calendar year will be lowered from 50 to five returns in respect of a particular type of information return.

- The mandatory electronic filing thresholds for corporate income tax returns (for taxation years beginning after 2021) and indirect tax returns for GST/HST registrants (other than for charities or selected listed financial institutions) will be eliminated for reporting periods beginning after 2021. Therefore, most corporations and GST/HST registrants will be required to file these returns electronically.

- The threshold requiring professional preparers of income tax returns to file electronically if they prepare more than 10 corporate or personal income tax returns (other than trusts) will be lowered to five of either type of return for a calendar year, and the exception for trusts will be removed. In addition, the exception that allows a tax preparer to file a maximum of 10 paper corporate and 10 personal income tax returns per calendar year will be lowered to a maximum of five paper returns of each type per calendar year, effective for the 2022 and later calendar years.

- Issuers of T4A (Statement of Pension, Retirement, Annuity and Other Income) and T5 (Statement of Investment Income) information returns will be able to provide them to taxpayers electronically without having to also issue a paper copy and without the taxpayer having to authorize the issuer to do so for T4A and T5 returns issued after 2021.

- The default method of correspondence for businesses that use the CRA’s My Business Account portal will be changed to electronic only in respect of various statutes, effective for the date the corresponding legislation receives Royal Assent (although businesses could still choose to also receive paper correspondence).

- The CRA will have the ability to send notices of assessment electronically without the taxpayer having to authorize the CRA to do so in respect of individuals who file their income tax returns electronically and those who employ the services of a tax preparer that files their income tax return electronically, effective for the date the corresponding legislation receives Royal Assent.

- Electronic payments will be required for remittances over $10,000 under the Income Tax Act, and the threshold for mandatory remittances to be made at a financial institution under the GST/HST portion of the Excise Tax Act, the Excise Act, 2001, the Air Travellers Security Charge Act and Part 1 of the Greenhouse Gas Pollution Pricing Act will be lowered from $50,000 to $10,000 for payments made on or after 1 January 2022. The budget also clarifies that payments required to be made at a financial institution under these statutes include online payments made through such an institution.

In addition, Budget 2021 proposes to eliminate the requirement for handwritten signatures, effective on the date the corresponding legislation receives Royal Assent, for the following forms:

- T183, Information Return for Electronic Filing of an Individual’s Income Tax and Benefit Return

- T183CORP, Information Return for Corporations Filing Electronically

- T2200, Declaration of Conditions of Employment

- RC71, Statement of Discounting Transaction

- RC72, Notice of the Actual Amount of the Refund of Tax

Employee ownership trusts

Budget 2021 announced that the government will consult with stakeholders on the barriers that exist to the creation of employee ownership trusts in Canada, and how workers and owners of private businesses in Canada can benefit from the use of employee ownership trusts. Employee ownership trusts are used in the United States and the United Kingdom to support and encourage employee ownership of a business and facilitate the transition of privately owned businesses to employees.

International tax measures

Transfer pricing

Identifying that the Federal Court of Appeal decision in Her Majesty The Queen v Cameco Corporation has “highlighted concerns with the application of Canada’s domestic transfer pricing rules,” the government is proposing to release a consultation document on enhancements to Canada’s transfer pricing rules. The documents are to be released in the coming months.

Base erosion and profit shifting

Budget 2021 proposes to further implement leading practices recommended by the Organisation for Economic Co-operation and the Group of 20 in the BEPS Action Plan, specifically in respect of interest deductibility limitations and hybrid mismatch arrangements.

Interest deductibility limits

Budget 2021 proposes to introduce a new earnings-stripping rule consistent with the recommendations in the Action 4 Report of the BEPS Action Plan. The new rule would limit the amount of net interest expense that a corporation may deduct in computing its taxable income to no more than a fixed ratio of “tax EBITDA.” Tax EBITDA is described to be a corporation’s taxable income before taking into account interest income and expense, income tax, and deductions for depreciation and amortization, where each of these items is as determined for tax purposes.

The new earnings-stripping rule would apply generally to Canadian corporations, trusts, partnerships and Canadian branches of nonresident corporations. Those exempted from the new rule would be limited to CCPCs that, together with any associated corporations, have taxable capital employed in Canada of less than $15 million, and groups of corporations and trusts whose aggregate net interest expense among their Canadian members is $250,000 or less.

For these purposes:

- EBITDA would exclude, among other things, dividends to the extent they qualify for the inter-corporate dividend deduction or the deduction for certain dividends received from foreign affiliates.

- Interest expense and interest income would include not only amounts that are legally interest, but also certain payments that are economically equivalent to interest, and other financing-related expenses and income.

- Canada’s existing thin capitalization rules will continue to apply. For the purposes of this earnings-stripping measure, the measure of interest expense would exclude interest that is not deductible under existing income tax rules, including the existing thin capitalization rules.

- Interest expense and interest income related to debts owing between Canadian members of a corporate group would generally be excluded.

The new earnings-stripping rule is to be phased in, with a fixed ratio of 40% of EBITDA for taxation years beginning on or after 1 January 2023 but before 1 January 2024 (the transition year) and 30% for taxation years beginning on or after 1 January 2024. The proposed measure also includes a “group ratio” rule that would allow a taxpayer to deduct interest in excess of the fixed ratio of tax EBITDA where the taxpayer is able to demonstrate that the ratio of net third-party interest to book EBITDA of its consolidated group implies that a higher deduction limit would be appropriate. For this purpose, the consolidated group would comprise the parent company and all of its subsidiaries that are fully consolidated in the parent’s audited consolidated financial statements. Measures of net third-party interest expense and book EBITDA under this rule would be based on the group’s audited consolidated financial statements with appropriate adjustments.

The rules should generally allow for the results among a Canadian group to be effectively combined. For example, interest expense and interest income between Canadian members of a corporate group will generally be excluded. Further, Canadian members of a group that have a ratio of net interest to tax EBITDA below the fixed ratio would generally be able to transfer the resultant unused capacity to deduct interest to other Canadian members of the group whose net interest expense deductions, including denied deductions carried over from another year, would otherwise be limited by the rule. (The definition of a “group” for these purposes was not clear and is to be included in the draft legislation.) This combining measure may have limited application to Canadian banks and life insurance companies, which may not be able to combine their net interest income from their regulated banks or insurance businesses against net interest expense for other members of their corporate group that are not regulated banking or insurance entities.

Interest denied under the earnings-stripping rule would be able to be carried forward for up to 20 years or back for up to three years. Denied interest would be allowed to be carried back to taxation years that begin prior to the effective date of the rule, to the extent that the taxpayer would have had the capacity to absorb these denied expenses, had the proposed rule been in effect for those years. In determining whether the taxpayer would have had the capacity to absorb the denied expenses in those years, any such capacity would be reduced by overall net interest expense, in aggregate for all those years, of Canadian members of the taxpayer’s group that exceeded the fixed ratio (or the group ratio, discussed below, if higher).

The government appears to expect that standalone Canadian corporations and members of groups consisting only of Canadian corporations would, in most cases, not have their interest expense deductions limited under the proposed rule. This is due to the combination of the group ratio rules and measures allowing for combining the Canadian results. Measures to reduce the compliance burden on these entities and groups will be explored.

As part of the phasing-in of the new earnings-stripping measure, taxpayers that have interest deductions denied for the transition year would be able to carry back and deduct the denied interest in any of the three preceding years, as discussed above, using the 40% fixed ratio (or the group ratio for that earlier year, if higher) to determine their capacity to absorb carried-back interest in those preceding years. Where interest deductions are denied for a year following the transition year, carrybacks of denied interest to the transition year or an earlier year would be allowed using the 30% fixed ratio (or the group ratio for the transition year or that earlier year, as the case may be, if higher) to determine their capacity to absorb carried-back interest in those preceding years.

This measure would apply to taxation years that begin on or after 1 January 2023 (with an anti-avoidance rule to prevent taxpayers from deferring the application of the measure) and would apply with respect to existing as well as new borrowings. Draft legislative proposals are expected to be released for comment in the summer.

Hybrid mismatch arrangements

Budget 2021 describes hybrid mismatch arrangements as cross-border tax avoidance structures that exploit differences in the income tax treatment of business entities or financial instruments under the laws of two or more countries to produce mismatches in tax results. The Action 2 report of the BEPS Action Plan details rules for countries to adopt in their domestic legislation with the objective of neutralizing tax benefits arising out of hybrid mismatch arrangements. Budget 2021 proposes to implement rules consistent with the Action 2 recommendations, with appropriate adaptations to the Canadian income tax context.

The supplemental information released with Budget 2021 identifies the following types of hybrid mismatch that were addressed in the BEPS Action 2 recommendations:

- Deduction/non-inclusion mismatches. These are where a country allows a deduction in respect of a cross-border payment, but where the corresponding receipt of the payment is not included in ordinary income within a reasonable time period in the other country.

- Double deduction outcomes. These outcomes arise where a tax deduction is available in two or more countries in respect of a single economic expense.

- Imported mismatches. Imported mismatches generally arise where a payment is deductible by an entity resident in one country and included in the ordinary income of the recipient entity, but where that ordinary income is reduced against a deduction under a hybrid mismatch arrangement between the second country and an entity resident in a third country.

- Branch mismatch arrangements. These arrangements occur where the resident country of a taxpayer takes a different view from that of the country where the taxpayer’s branch is located in respect of how income and expenditures between the two countries are to be allocated.

Budget 2021 will introduce rules to neutralize hybrid mismatch arrangements in two separate legislative packages. The first package will be released for stakeholder comment later in 2021, and those rules will apply as of 1 July 2022. The second package will be released for stakeholder comment after 2021, and those will apply no earlier than 2023.

The first legislative package would appear to address rules specific to hybrid instruments and will rely on recommendations in Chapters 1 and 2 of the Action 2 report. The measures would appear to address both an inbound situation, such as where a Canadian taxpayer makes an otherwise deductible payment that is not included in ordinary income in the hands of the nonresident recipient, and an outbound situation, such as where a Canadian taxpayer receives a payment that was deductible in the hands of a nonresident payer but to which the Canadian taxpayer may claim an exemption.

In general terms, under the main proposed rules, payments made by Canadian residents under hybrid mismatch arrangements would not be deductible for Canadian income tax purposes to the extent that they give rise to a further deduction in another country or are not included in the ordinary income of a nonresident recipient. Conversely, to the extent that a payment made under such an arrangement by an entity that is not resident in Canada is deductible for foreign income tax purposes, no deduction in respect of the payment would be permitted against the income of a Canadian resident. Any amount of the payment received by a Canadian resident would also be included in income and, if the payment is a dividend, it would not be eligible for the deduction otherwise available for certain dividends received from foreign affiliates. In effect, these rules would neutralize a mismatch by aligning the Canadian income tax treatment with the income tax treatment in the foreign country.

The proposed rules would be a “results-based” test that would not be conditioned on a purpose test. The rules should generally apply in respect of payments between related parties and payments under certain “structured arrangements” between unrelated parties that are designed to produce a mismatch. The proposed rules also contain ordering rules, as recommended in the BEPS Action 2 report, to be coordinated with similar rules in other countries.

The second legislative package will address hybrid mismatch arrangement rules not addressed in the first package. These may include branch mismatch arrangements, imported mismatch arrangements and reverse hybrids, to be introduced to the extent relevant and appropriate in the Canadian context.

Tax on unproductive use of Canadian housing by foreign nonresident owners

Budget 2021 proposes an annual 1% tax on vacant or underused residential properties owned by nonresident, non-Canadian persons.

In its 2020 fall economic statement, the government announced that it would take steps to implement a national, tax-based measure targeting the unproductive use of domestic housing that is owned by nonresident non-Canadians. This measure is intended as a tool to assist in maintaining the affordability of residential housing for Canadians.

In Budget 2021, the federal government announced its intention to implement a national, annual 1% tax on the value of nonresident, non-Canadian-owned residential real estate that is considered to be vacant or underused, effective 1 January 2022. The tax would require all owners, other than Canadian citizens or permanent residents of Canada, to file a declaration as to the current use of the property, with significant penalties for failure to file.

Beginning in 2023, all owners of residential property in Canada, other than Canadian citizens or permanent residents of Canada, would be required to file an annual declaration for the prior calendar year with the CRA in respect of each Canadian residential property they own. The requirement to file an annual declaration would apply irrespective of whether the owner is subject to tax in respect of the property for the year. In the declaration, the owner would be required to report information such as the property address, the property value and the owner’s interest in the property. The owner may be eligible to claim an exemption from the tax in respect of a property for the year. An exemption may be available, for instance, where a property is leased to one or more qualified tenants in relation to the owner for a minimum period in a calendar year. Where an exemption in respect of a property for the year is not available, the owner would be required to calculate the amount of tax owing and report and remit it to the CRA by the filing due date. The failure to file a timely declaration with respect to a property for a calendar year could result in the loss of any available exemptions in respect of the property for the year. Penalties and interest would also be applicable, and the assessment period would be unlimited.

The government intends to release a consultation paper in the coming months to provide stakeholders with an opportunity to comment on the parameters of the proposed tax, including on whether special rules should be established for small tourism and resort communities. It is estimated this measure will increase federal revenues by $700 million over four years, starting in 2022–23.

Anti-avoidance measures

Mandatory disclosure rules

Budget 2021 outlines broad proposals to enable the CRA to have better visibility of transactions or tax reduction planning that they would consider aggressive in nature. The proposals are based on the principles set out in the Organisation for Economic Co-operation and Development (OECD) project to identify base erosion and profit shifting, Action 12: Final Report.

The proposals are focused on:

- Strengthening of the existing reportable transaction rules

- New reporting requirements for a prescribed listing of notifiable transactions

- New rules to require larger corporations to report to CRA all “uncertain tax treatments” that were required to be disclosed in their audited financial statements

- The indefinite extension of the reassessment periods and penalties for non-compliance, including the expansion or introduction of reporting requirements and penalties for most professional tax advisors and promoters

It is proposed that the new rules will be effective in 2022 following the release of draft legislation in the coming weeks and a consultation period that will end on 3 September 2021.

Reportable transactions

The Income Tax Act currently contains rules that require that certain transactions entered into by a taxpayer be reported to the CRA. For a transaction to be reportable under those rules, it must be an “avoidance transaction,” as that term is defined for the purposes of the general anti-avoidance rule in the Income Tax Act. As well, the transaction must bear at least two of three generic hallmarks:

- A promoter or tax advisor in respect of the transaction is entitled to fees, often referred to as “contingent fees.”

- A promoter or tax advisor requires “confidential protection” with respect to the transaction.

- The taxpayer, or the person who entered into the transaction for the benefit of the taxpayer, obtains “contractual protection” in respect of the transaction.

While the current rules were intended to provide the CRA with information on transactions with the identified hallmarks, they have resulted in limited reporting by taxpayers. Amendments to the reportable transaction rules are proposed to increase reporting under the mandatory disclosure rules and to bring them in line with international leading practices.

In particular, it is proposed that only one generic hallmark be met in order for a transaction to be reportable. It is also proposed that the definition of “avoidance transaction” for these purposes be amended so that a transaction be considered an avoidance transaction if it can reasonably be concluded that one of the main purposes of entering into the transaction is to obtain a tax benefit.

It is proposed that a taxpayer who enters into a reportable transaction, or another person who enters into such a transaction in order to procure a tax benefit for the taxpayer, would be required to report the transaction to the CRA within 45 days of the earlier of:

- The day the taxpayer becomes contractually obligated to enter into the transaction or a person who entered into the transaction for the benefit of the taxpayer becomes contractually obligated to enter into the transaction; or

- The day the taxpayer enters into the transaction or a person who entered into the transaction for the benefit of the taxpayer enters into the transaction.

It is further proposed that reporting (as a reportable transaction) of a scheme that, if implemented, would be a reportable transaction be required to be made by a promoter or advisor (as well as by persons who do not deal at arm’s length with the promoter or advisor and who are entitled to receive a fee with respect to the transaction) within the same time limits. It is proposed that an exception to the reporting requirement be available for advisors to the extent that solicitor-client privilege applies.

Notifiable transactions

To provide the CRA with pertinent information relating to tax avoidance transactions (including series of transactions) and other transactions of interest on a timely basis, it is proposed, similar to Quebec’s recently released “specified transactions,” to introduce a category of specific hallmarks known as “notifiable transactions.” These notifiable transactions would be designated by the Minister of National Revenue with the concurrence of the Minister of Finance. No specific list of notifiable transactions was released in the budget documents.

The reporting requirements of taxpayers and promoters for notifiable transactions are proposed to mirror those previously noted.

Uncertain tax treatments

An uncertain tax treatment is a tax treatment used, or planned to be used, in an entity’s income tax filings for which there is uncertainty over whether the tax treatment will be accepted as being in accordance with tax law. At present, there is no requirement in Canada to disclose uncertain tax treatments.

It is proposed that specified corporate taxpayers be required to report particular uncertain tax treatments to the CRA. A reporting corporation would generally be required to report an uncertain tax treatment in respect of a taxation year where the following conditions are met:

- The corporation is required to file a Canadian return of income for the taxation year. That is, the corporation is a resident of Canada or is a nonresident corporation with a taxable presence in Canada.

- The corporation has at least $50 million in assets at the end of the financial year that coincides with the taxation year (or the last financial year that ends before the end of the taxation year). This threshold would apply to each individual corporation.

- The corporation, or a related corporation, has audited financial statements prepared in accordance with IFRS or other country-specific GAAP relevant for domestic public companies (e.g., US GAAP).

- Uncertainty in respect of the corporation’s Canadian income tax for the taxation year is reflected in those audited financial statements (i.e., the entity concluded it is not probable that the taxation authority will accept an uncertain tax treatment and thus, as described by the IFRS Interpretations Committee, it is probable that the entity will receive or pay amounts relating to the uncertain tax treatment).

For each reportable uncertain tax treatment of a corporation, the corporation would be required to provide prescribed information, such as the quantum of taxes at issue, a concise description of the relevant facts, the tax treatment taken (including the relevant sections of the Income Tax Act) and whether the uncertainty relates to a permanent or temporary difference in tax.

It is proposed that uncertain tax treatments be required to be reported at the same time that the reporting corporation’s Canadian income tax return is due.

Reassessment period

It is proposed that, where a taxpayer has a reporting requirement in respect of a transaction relevant to the taxpayer’s income tax return for a taxation year, the normal reassessment period would not commence in respect of the transaction until the taxpayer has complied with the reporting requirement. As a result, if a taxpayer does not comply with a mandatory disclosure reporting requirement for a taxation year in respect of a transaction, a reassessment of the year in respect of the transaction would not become statute barred.

Taxpayer penalty

It is proposed that, with respect to persons who enter into reportable or notifiable transactions, or for whom a tax benefit results from a reportable or notifiable transaction, a penalty of $500 per week apply for each failure to report a reportable transaction or a notifiable transaction, up to the greater of $25,000 and 25% of the tax benefit, or for corporations that have assets that have a total carrying value of $50 million or more, a penalty of $2,000 per week, up to the greater of $100,000 and 25% of the tax benefit.

Promoter penalty

It is also proposed that, with respect to advisors and promoters of reportable or notifiable transactions, as well as with respect to persons who do not deal at arm’s length with them and who are entitled to a fee with respect to the transactions, a penalty be imposed for each failure to report equal to the total of:

- 100% of the fees charged by that person to a person for whom a tax benefit results;

- $10,000; and

- $1,000 for each day during which the failure to report continues, up to a maximum of $100,000.

Uncertain tax treatment penalty

For corporations subject to the requirement to report uncertain tax treatments, it is proposed that the penalty for failure to report each particular uncertain tax treatment be $2,000 per week, up to a maximum of $100,000.

Avoidance of tax debts

Budget 2021 proposes several measures to address the perceived abusive arrangements designed to avoid joint and several liability for taxes on the non-arm’s length transfer of property (tax debt avoidance rule), as well as a penalty for those who devise and promote these schemes.

Specifically, the proposals introduce anti-avoidance rules (i) deeming a tax debt to have arisen before the end of the taxation year of a transfer of property, (ii) deeming the transferor and transferee, who are dealing at arm’s length, to be deemed not to be dealing at arm’s length, and (iii) requiring the overall result of the series of transactions to be considered in determining the values of properties transferred.

A penalty is proposed for advisors and promoters of tax debt avoidance schemes. The rules would apply in respect of transfers of property that occur on or after 19 April 2021.

Audit authorities

A recent Tax Court decision called into question whether the CRA can require persons to fully co-operate in providing oral and written information during a tax audit. The budget proposes to introduce enhanced rules that would give the CRA the authority it needs to conduct audits and other compliance activities under the various acts dealing with numerous taxes and federal charges.

Tax measures for individuals and trusts

Personal income tax rates

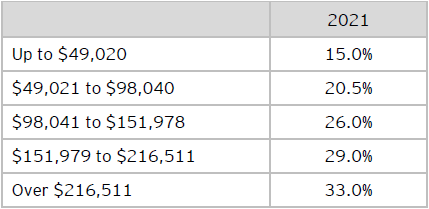

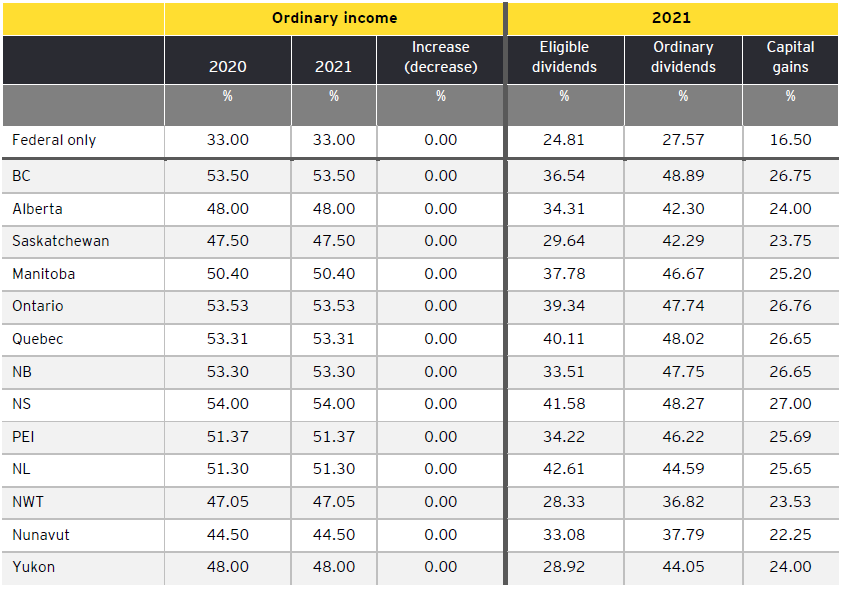

There are no individual income tax rate or tax bracket changes in this budget. The brackets will continue to be indexed for inflation. See Table B for the 2021 federal rates and the Appendix for the top combined marginal rates by province and territory.

Table B: Federal personal income tax rates

Tax credit changes

Budget 2021 includes the following refundable and non-refundable tax credit proposals:

Canada workers benefit

Budget 2021 proposes to enhance the Canada workers benefit (CWB), a refundable tax credit aimed at supplementing the earnings of low- and modest-income workers, for 2021 and later taxation years, as follows:

- The rate at which the CWB grows will be increased from 26% to 27% for every dollar of “working income” (generally employment and business income) in excess of $3,000, up to a maximum entitlement of $1,395 for single individuals without dependants and $2,403 for families. A corresponding change will be made to the disability supplement phase-in rate.

- The income thresholds at which the CWB begins to be phased out are increased from $13,194 to $22,944 for single individuals without dependants and from $17,522 to $26,277 for families. In addition, the phase-out rate will increase from 12% to 15% of adjusted net income in excess of the proposed thresholds. Corresponding changes will be made to the disability supplement phase-out income threshold and rate.

- A secondary earner exemption will be introduced to allow the spouse or common-law partner with the lower working income to exclude up to $14,000 of their working income from their adjusted net income for purposes of the CWB phase-out.

- Indexation of amounts relating to the CWB, including the secondary earner exemption amount, will continue to apply after the 2021 taxation year.

Disability tax credit

To qualify for the disability tax credit (DTC), an individual must have one or more severe and prolonged impairments in physical or mental functions. The effects of the impairment must be such that the individual’s ability to perform a basic activity of daily living is markedly restricted or would be without life-sustaining therapy. Basic activities of daily living are defined to include “mental functions necessary for everyday life.” Under current rules, the definition of “life-sustaining therapy” includes the requirement that it be administered at least three times a week for an average of at least 14 hours each week.

Budget 2021 proposes a number of technical changes to improve access to the DTC and other tax-related measures requiring a DTC certificate as follows:

- The list of “mental functions necessary for everyday life” will be expanded.

- The requirement for therapy to be administered at least three times each week will be reduced to two times each week.

- The list of activities allowed to be counted as time spent receiving “life-sustaining therapy” will be expanded and clarified to recognize certain components of therapy that are excluded under current rules.

- In addition, where an individual is incapable of performing therapy on their own, the proposal will allow time required by another person to assist in the therapy to be counted.

Other personal tax measures

Tax treatment of COVID-19 benefit amounts

Individuals who must repay certain COVID-19 benefits may only claim a deduction in the year of repayment. Since COVID-19 benefits are taxable in the year of receipt, under current rules the income inclusion and related tax liability may be in a different year than the deduction for repayment. Budget 2021 proposes to allow individuals who repay certain COVID-19 benefits before 2023 to claim a deduction in computing income for the year in which the benefit was received, rather than in the year the repayment was made. If the individual makes the repayment after filing their income tax return reporting the income inclusion, the proposal allows the individual who claimed the deduction to be able to file an adjustment.

Budget 2021 also proposes to include COVID-19 benefits received by individuals who are considered nonresident persons for income tax purposes in their taxable income earned in Canada.

Postdoctoral fellowship income

Budget 2021 proposes to include postdoctoral fellowship income in “earned income” for the purpose of determining an individual’s contribution limit for a registered retirement savings plan (RRSP). The proposal, which will apply in respect of postdoctoral fellowship income received in 2021 and subsequent years, will also allow a taxpayer to request an adjustment to their RRSP room in respect of postdoctoral fellowship income received from 2011 to 2020.

Northern residents deduction

Budget 2021 proposes to expand access to the travel component of the northern residents deduction to northern resident taxpayers without employer-provided travel benefits. For 2021 and later taxation years, residents of northern zones will have the option to claim (in respect of themselves and each eligible family member) the amount of employer-provided travel benefits received or up to a standard amount of $1,200. The standard amount is reduced to $600 in the case of residents of intermediate zones.

Defined contribution pension plans: fixing contribution errors

The 2021 federal budget proposes to permit plan administrators of defined contribution pension plans to correct for both undercontributions and overcontributions as follows:

- Additional contributions to an employee’s account under a defined contribution pension plan may be made to compensate for an undercontribution error made in any of the preceding five years, subject to a dollar limit. The additional contributions would reduce the employee’s RRSP contribution room for the taxation year following the year in which the retroactive contribution is made (if the reduction results in negative RRSP room, it will only impact the employee’s contributions made in future years).

- Excess amounts may be refunded to the employee or employer (as the case may be) who made the contribution to correct for a pension overcontribution error in any of the five years prior to the year in which the amount was refunded. Refunds of overcontributions would generally restore the employee’s RRSP contribution room for the taxation year in which the refund is made.

The plan administrator will be required to file a prescribed form in respect of each affected employee, rather than amend prior-year T4 slips. These measures apply in respect of additional contributions made, and amounts of overcontribution refunded, in 2021 and later taxation years.

Taxes applicable to registered investments

The 2021 federal budget announced a more equitable method of applying the Part X.2 penalty tax to trusts or corporations that are registered investments. Part X.2 tax is targeted at ensuring certain registered investments are holding the same properties as the registered plans they are authorized for, by imposing a penalty tax equal to 1% of the fair market value of a non-qualified investment at the time it was acquired, for each month the investment is held. The tax is currently applied without consideration to the extent registered plans are invested in units or shares of the registered investment. The amendment will prorate any Part X.2 tax, limiting it to the proportion of the registered investment held by registered accounts.

This amendment generally applies after 2020. However, it may also apply retroactively to months prior to 2021, provided the CRA has not finally determined the Part X.2 tax in respect of the pre-2021 months as of 19 April 2021.

Increasing Old Age Security for Canadians 75 and over

Budget 2021 proposes the following changes to increase Old Age Security for Canadians who are age 75 and older:

- Old Age Security pensioners who will be age 75 or older as of June 2022 will receive a taxable grant payment of $500 in August 2021.

- This payment will be exempt from the definition of income for the Guaranteed Income Supplement.

- Maximum benefits payable to Old Age Security pensioners age 75 and older will be increased by 10% effective 1 July 2022.

Other personal measures

Extension of Canada recovery benefits

The 2021 federal budget proposes to extend the Canada Recovery Benefit (CRB) by providing up to 12 additional weeks of income support to claimants who will begin exhausting their 38 weeks of CRB support on 19 June 2021. The benefit payment will be equal to $500 per week for the first four additional weeks and will then be reduced to $300 per week for the remaining eight additional weeks. All new CRB claimants after 17 July 2021 will receive the lower weekly rate of $300 up until 25 September 2021. In addition, the budget proposes to extend the Canada Recovery Caregiving Benefit (CRCB) by an additional four weeks, up to a maximum of 42 weeks, at $500 per week.

The government will also seek legislative authority to make further extensions, as necessary, to the CRB-related supports (including the CRCB and the Canada Recovery Sickness Benefit) and EI regular benefits up until 20 November 2021.

Charities and non-profit organizations

Budget 2021 proposes the following measures relating to charities.

Preventing abuse of charitable registration status for terrorist financing purposes

- Allows the Minister to immediately revoke the charitable status of a registered charity or other qualified donee should it become a listed terrorist entity under the Criminal Code.

- Prevents individuals with a known history of supporting terrorism from becoming directors, trustees or similar officials of registered charities by expanding the definition of an ineligible individual. An ineligible individual will include a listed terrorist entity or a member of a listed terrorist entity, as well as a director, trustee, officer or like official of a listed terrorist entity, or an individual who controlled or managed, directly or indirectly, in any manner whatsoever, a listed terrorist entity during a period in which that entity supported or engaged in terrorist activities.

Potential increase to the disbursement quota of registered charities

- Launches public consultations on potentially increasing the disbursement quota, or minimum annual spending requirement, of charities to ensure that grant-making and spending on charitable activities keep pace with growth in charities’ investment assets.

False statements made for the purpose of maintaining charitable registration

- Allows the Minister to suspend a charity’s ability to issue official donation receipts for one year or to revoke an organization’s charitable status where a false statement amounting to culpable conduct was made for the purpose of maintaining charitable registration. The rules currently allow for revocation of charitable status where a false statement is made for the purpose of obtaining charitable registration.

No new measures were introduced in Budget 2021 relating to non-profit organizations.

Sales and excise tax legislative amendments

GST/HST measures

Application of the GST/HST to e-commerce and digital services tax

On 30 November 2020, the federal government tabled Supporting Canadians and Fighting COVID-19: Fall Economic Statement 2020. The fall economic statement (FES) contains significant GST/HST proposals, including measures designed to ensure that GST/HST applies fairly and effectively in the context of an increasingly digital economy. Specifically, nonresident vendors supplying services and digital products to consumers in Canada would be required to register for, collect and remit GST/HST.

Similar requirements would apply to supplies of short-term accommodation made through digital accommodation platforms, as well as to goods supplied through fulfillment warehouses. Draft legislation to implement these proposals was issued for public consultation.

For more information regarding the FES, please refer to EY Tax Alert 2020 Issue No. 58.

Revised legislation was released with Budget 2021 that incorporated changes taking into account comments received from stakeholders:

Safe Harbour Rules for Platform Operators: Under the proposed amendments, platform operators who facilitate sales by third-party suppliers will be jointly and severally, or solidarily, liable for the collection and remittance of GST/HST. However, if the third-party supplier provides false information to the platform operator and the platform operator reasonably relied on the information provided by a third-party supplier, the platform operator will be relieved from liability. This would ensure that a platform operator is not held liable for failing to collect and remit tax by relying in good faith on the information provided by a third-party supplier. The liability for amounts of tax not collected would be on the third-party supplier that provided false information.

Eligible deductions: Budget 2021 clarifies that suppliers registered for GST/HST under the simplified framework are eligible to deduct amounts for bad debts and certain provincial HST point-of-sale rebates provided to purchasers, and that public libraries and similar institutions are eligible to claim a rebate for the GST paid on audiobooks acquired from suppliers registered under the simplified system.

Threshold amount determination: Budget 2021 further proposed to amend the draft legislation to clarify that consideration receivable for zero-rated supplies (i.e., taxable at a rate of 0%) is not included in the $30,000 threshold amount for determining if a person is required to be registered for the GST/HST under the new registration rules. In addition, Budget 2021 clarifies that sales made on board aircraft or vessels engaged in international passenger transportation will be excluded from the new registration requirements.

Platform operator information return: Budget 2021 clarifies that the requirement to file an annual information return applies only to platform operators that are registered or required to be registered for the GST/HST.

Authority for the Minister of National Revenue to register a person: Budget 2021 proposes to grant the Minister of National Revenue authority to register a person that the Minister believes should be registered under the new registration rules. The Minister of National Revenue is already allowed under the existing GST/HST registration rules to make such a determination.

The proposals are expected to come into force starting 1 July 2021. During a 12-month transition period starting from the effective date, the CRA will take a practical approach to compliance and exercise discretion in administering these measures.

Input tax credit information requirements

Businesses can claim input tax credits (ITCs) to recover the GST/HST they pay for goods and services used as inputs in their commercial activities. To support their ITC claims, businesses must obtain and retain information that is contained in supporting documentation (e.g., invoices, receipts) provided by their suppliers. The information requirements for these documents are graduated with progressively more information required when the amount paid or payable in respect of a supply equals or exceeds thresholds of $30 or $150. Depending on the amount paid or payable in respect of the supply, either the supplier or the intermediary must provide its business name and its GST/HST registration number. Currently, the term “intermediary” defined in section 2 of the Input Tax Credit Information (GST/HST) Regulations does not include a billing agent.

Budget 2021 proposes to increase the current ITC information thresholds to $100 (from $30) and $500 (from $150) and to allow billing agents to be treated as intermediaries for purposes of the required ITC information.

These measures would come into force on 20 April 2021.

GST new housing rebate conditions

The GST new housing rebate entitles homebuyers to recover 36% of the GST (or the federal component of the HST) paid on the purchase of a new home priced up to $350,000 when certain conditions are met. The rebate is then phased out for between $350,000 and $450,000, with no federal rebate available on homes above this price.

One of the conditions is that the purchaser must acquire the new home for use as their primary place of residence or as the primary place of residence of a relation. Currently, if two or more individuals who are not considered to be related buy a new home together, each of them must meet this condition.

Budget 2021 addresses this issue. The GST new housing rebate will now be available as long as the new home is acquired for use as the primary place of residence of any one of the purchasers or a relation of any one of the purchasers.

This measure would apply to a supply made under an agreement of purchase and sale entered into after 19 April 2021.

Digital services tax

In addition to imposing GST/HST registration, collection and remittance requirements on nonresident vendors and nonresident digital platform operators, the federal government proposed in its FES to implement a new tax on corporations providing digital services.

Budget 2021 provides more details about this new tax that is proposed to be applicable at a rate of 3% on revenue from certain digital services reliant on the engagement, data and content contributions of Canadian users. This digital services tax is proposed to apply starting 1 January 2022, until an acceptable multilateral option takes effect (e.g., a multilateral solution under the auspices of the OECD).

No draft legislative proposals were announced with respect to the digital services tax, and Budget 2021 indicates that Canada will provide the OECD until the summer of 2021 to reach a consensus on this issue, absent which Canada will move to introduce the digital services tax on 1 January 2022. The government invites input from stakeholders.

Excise duty measures

Rebate of excise tax for goods purchased by provinces

Under the Excise Tax Act, provinces are provided relief from the federal excise tax embedded in the price of motive fuels, air conditioners in automobiles and fuel-inefficient vehicles, which they purchase or import for the province’s own use. The provincial-use rebate is available and could be claimed by the province itself or by the vendor when the province does not have an agreement with the federal government where, inter alia, the province and the federal government mutually agree to pay each other’s taxes.

Budget 2021 proposes to create a joint election mechanism to specify that the vendor alone would be eligible to apply for the rebate only if it jointly elects with the province to be the eligible party. This measure would apply in relation to goods purchased or imported by a province on or after 1 January 2022.

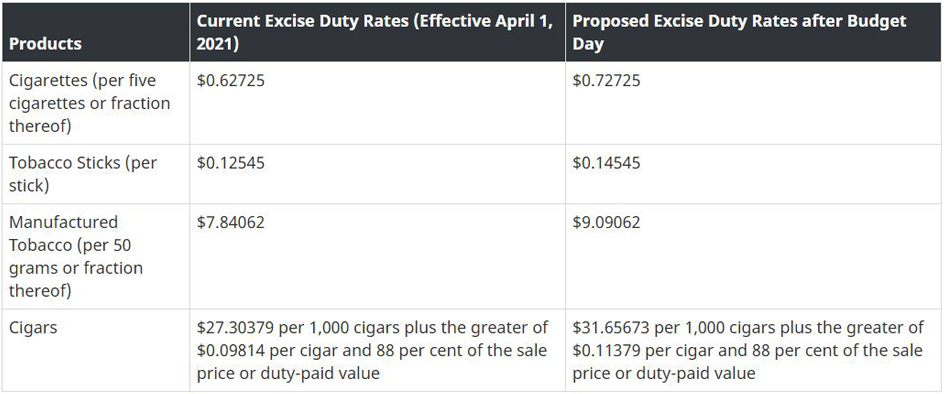

Excise duty on tobacco

Budget 2021 proposes to increase the tobacco excise duty rate by $4 per carton of 200 cigarettes, along with corresponding increases to the excise duty rates for other tobacco products, effective 20 April 2021.

Tobacco Excise Duty Rate Stucture

Manufacturers, importers, wholesalers and retailers are required to pay an inventory tax of $0.02 per cigarette on hand as of 12:01 am 20 June 2021, subject to certain exemptions, and until 30 June 2021 to file a return and pay this inventory tax.

Excise duty on vaping products

Budget 2021 proposes to implement an excise duty on vaping products in 2022 under the framework of the existing Excise Act, 2001. The new duty would apply solely to vaping liquids that are produced in Canada or imported and that are intended for use in a vaping device in Canada. The proposed rate duty would be $1.00 per 10 ml, or fraction thereof, and would be calculated and imposed based on the volume of the smallest immediate container holding the liquid.

Similar to excise duty on tobacco and other products, manufacturers and importers of dutiable vaping products would be required to obtain an excise licence, and a package stamping regime similar to that used for cigarettes will be imposed showing that duties have been paid on products held for retail sale.

The federal government intends to work collaboratively with any provinces and territories that may be interested in a federally coordinated approach to taxing the vaping products.

Tax on select luxury goods

Budget 2021 proposes to introduce a tax on the retail sale of new luxury cars and personal aircraft priced over $100,000 and boats priced over $250,000, effective as of 1 January 2022. For vehicles, aircraft and boats sold in Canada, the tax would apply at the point of purchase if the final sale price paid by a consumer (not including the GST/HST or provincial sales tax) is above $100,000 or $250,000, as the case may be. Importations of vehicles, aircraft and boats would also be subject to the tax.

For vehicles and aircraft priced over $100,000, the amount of the tax would be the lesser of 10% of the full value of the vehicle or the aircraft, or 20% of the value above $100,000. For boats priced over $250,000, the amount of the tax would be the lesser of 10% of the full value of the boat or 20% of the value above $250,000.

Customs measures

Budget 2021 contains several proposals to support Canadian international trade, modernize customs infrastructure, and strengthen Canada’s trade remedy system and trade controls:

Improving duty and tax collection on imported goods

- Budget 2021 proposes changes to the Customs Act to improve duty and tax collection.

- Currently, some importers with foreign ties value their goods at a lower price than most Canadian importers by using a previous foreign sale price. This practice results in a lower value of duties and taxes paid when importing these goods into Canada. The amendments to the Customs Act and related regulations would ensure that all importers value their goods using the value of the last sale for export to a purchaser in Canada, ensuring fairness for all importers and enhancing consistency with international rules.

- These changes would generate an estimated $150 million in additional annual duty revenues.

- The changes would also modernize and digitize the duty and tax payment process for commercial importers to minimize administrative burden. These changes involve supporting the implementation and enforcement of a streamlined and harmonized billing cycle for commercial importations that will include flexibility to make good-faith corrections without incurring penalties or interest.

- These changes would coincide with implementation of key functionalities of the Canada Border Services Agency (CBSA) Assessment and Revenue Management initiative that is set to serve as a single portal for commercial importers.

Modernization of travel and trade

- Budget 2021 proposes to provide $656.1 million over five years, beginning in 2021–22, and $123.8 million ongoing, to the CBSA to improve the border experience for travellers, enhance the CBSA’s ability to detect contraband and help protect the integrity of Canada’s border infrastructure.

- Funding will also support three Canadian preclearance pilots in the United States that would enable customs and immigration inspections to be completed before goods and travellers enter Canada.

Strengthening Canada’s trade remedy system

- Budget 2021 announces the government’s intention to launch public consultations on measures to strengthen Canada’s trade remedy system and to improve access for workers and small and medium-sized enterprises. This may result in proposed amendments to the Special Import Measures Act and the Canadian International Trade Tribunal Act.

Administration of trade controls

- The government has been taking steps to bolster its system of trade controls to ensure that Canada effectively manages the cross-border flow of sensitive goods. This includes strengthening Canada’s oversight of the movement of prohibited firearms and arms exports, and additional monitoring and controls for imports of certain steel and aluminum products and supply-managed goods to better monitor trade flows.

- Budget 2021 proposes to provide $38.2 million over five years, starting in 2021–22, and $7.9 million per year ongoing, to Global Affairs Canada, as additional resourcing to support Canada’s trade controls regime.

Supports for exporters

- Budget 2021 announces the government’s intention to work with Export Development Canada to enhance supports to small and medium-sized exporters and to strengthen human rights considerations in export supports. The government may propose amendments to the Export Development Act.

Pending legislation

The government will proceed with the following pending legislative and regulatory proposals and other previously announced measures, modified to take into account consultations and deliberations since their release.

Income tax

- Draft legislative proposals for a new CEWS elective alternative baseline remuneration period re the three new CEWS/CERS qualifying periods (from 14 March to 5 June 2021) (3 March 2021)

- Draft legislative proposals regarding the CEWS/CERS reduction-in-revenue deeming rule and increased accessibility to CERS lockdown support (24 February 2021)

- Draft legislative proposals regarding deductions for child care expenses and disability supports for 2020 and 2021 (19 January 2021)

- 2021 automobile deduction limits announcement (21 December 2020)

- Automobile standby charge and operating expense benefit draft legislative proposals for 2020 and 2021 (21 December 2020)

- Draft legislative proposals regarding flow-through shares rules amendments first announced 10 July 2020 (16 December 2020) [refer to EY Tax Alert 2020 Issue 63]

- Draft legislative proposals regarding zero-emission vehicles new class 56 first announced 2 March 2020 and expansion of eligibility for classes 54 and 55 (15 December 2020)

- Bill C-14, Economic Statement Implementation Act 2020, regarding additional Canada Child Benefit payments for 2021 (first announced in the 2020 Fall Economic Statement) and CERS technical amendments on qualifying rent expenses (third reading and adoption by the House of Commons: 15 April 2021)

- Draft legislative proposals regarding 2020 Fall Economic Statement measures dealing with employee stock options (in replacement of the 17 June 2019 proposals), registered disability savings plans (in replacement of the 30 July 2019 proposals) and agricultural cooperatives patronage dividends paid in shares (30 November 2020) [refer to EY Tax Alert 2020 Issues 57 and No. 59]

- Remaining measures from the 2020 Fall Economic Statement (30 November 2020) [refer to EY Tax Alert 2020 Issue No. 57]

- Modernization of the anti-avoidance rules (including GAAR)

- Draft legislative proposals relating to employee life and health trusts (27 November 2020)

- Draft amending regulations regarding temporary relief from certain requirements related to registered pension plans and deferred salary leave plans (2 July 2020)

- Draft legislative proposals regarding the Canadian journalism labour tax credit, the criteria for qualified Canadian journalism organization status, and the digital news subscription tax credit (17 April 2020)

- Final list of prescribed drought regions for 2019 (18 February 2020)

- Draft legislative proposal relating to amateur athlete trusts (20 December 2019)

- 2020 automobile deduction limits announcement (19 December 2019)

- Notice of ways and means motion regarding the increase in the basic personal amount from $12,298 to $15,000 by 2023 for those earning less than, or equal to, the amount at which the 29% tax bracket begins (i.e., $150,473 in 2020 and $151,978 in 2021) and other related or consequential changes (9 December 2019)

- Draft legislative proposals relating to shared-custody parent — clarification of Canada Child Benefit and GST/HST credit eligibility (29 August 2019)

- Draft legislative proposals relating to the remaining measures from the 2019 federal budget (including foreign affiliate dumping, cross-border securities arrangements, transfer pricing, mutual funds “allocation to redeemers” methodology, additional types of permitted annuities for registered plans, extended reassessment period, and electronic delivery of requirements for information) and certain technical revisions from measures enacted in Bill C-97 (2019) (regarding CCA and resources expenses) (30 July 2019) [refer to EY Tax Alert 2019 Issue No. 30]

- 2019 automobile deduction limits announcement (27 December 2018)

- Final list of prescribed drought regions for 2018 (31 October 2018)

- Remaining measures from the 2018 federal budget (tabled 27 February 2018) and from the related 27 July 2018 draft legislation [refer to EY Tax Alerts 2018 Issues 7 and No. 31]

- New reporting requirements for trusts

- 2018 automobile deduction limits announcement (22 December 2017)

Indirect taxes

- Proposed Greenhouse Gas Offset Credit System Regulations (Canada) under the Greenhouse Gas Pollution Pricing Act (GGPPA) (6 March 2021).

- Draft legislative proposals regarding 2020 fall economic statement remaining measures dealing with the zero-rating of face masks and face shields (30 November 2020) [refer to EY Tax Alert 2020 Issue No. 58].

- Draft regulations amending various regulations relating to Part I of the GGPPA allowing Alberta TIER facilities to obtain fuel without federal fuel charge applying (6 December 2019).

- Draft legislative proposals relating to the remaining measures from the 2019 federal budget (30 July 2019) [refer to EY Tax Alert 2019 Issue No. 30].

- Draft legislative proposals relating to holding corporations, drop shipment rules, virtual currencies and freight transportation services (17 May 2019) [refer to EY Tax Alert 2019 Issue No. 24].

- Remaining measures from the 2018 federal budget (tabled 27 February 2018) and from the related 27 July 2018 draft legislation [refer to EY Tax Alert 2018 Issues 7 and No. 31].]

- GST/HST regulatory change regarding printed books rebate

- Remaining measures from the 2016 federal budget (tabled 22 March 2016)

- GST/HST joint venture election (stemming from the 2014 proposals under the previous government)

Webcasts

19 April 2021 webcast: The evening following the finance minister’s address, members of the EY Tax team will record their analysis and insights on the tax measures in the 2021 budget. View our webcast at ey.com/ca/Budget.

Learn more

For more information on the above measures or any other topics that may be of concern, contact your EY or EY Law advisor. And for up-to-date information on the federal, provincial and territorial budgets, visit ey.com/ca/Budget.

Download this tax alert

Appendix

Maximum combined personal marginal income tax rates (as at 19 April 2021)

Budget information: For up-to-date information on the federal, provincial and territorial budgets, visit ey.com/ca/Budget.